The Hardest Part of Homeownership Today Is Not the Mortgage. It Is Getting Through the Front Door.

Why This Matters More Than Most People Realize

For years, Americans were told some version of the same story: buy a home when you can, build equity over time, and let that equity become part of your long-term financial foundation. That basic idea is still true. What has changed is the difficulty of getting started.

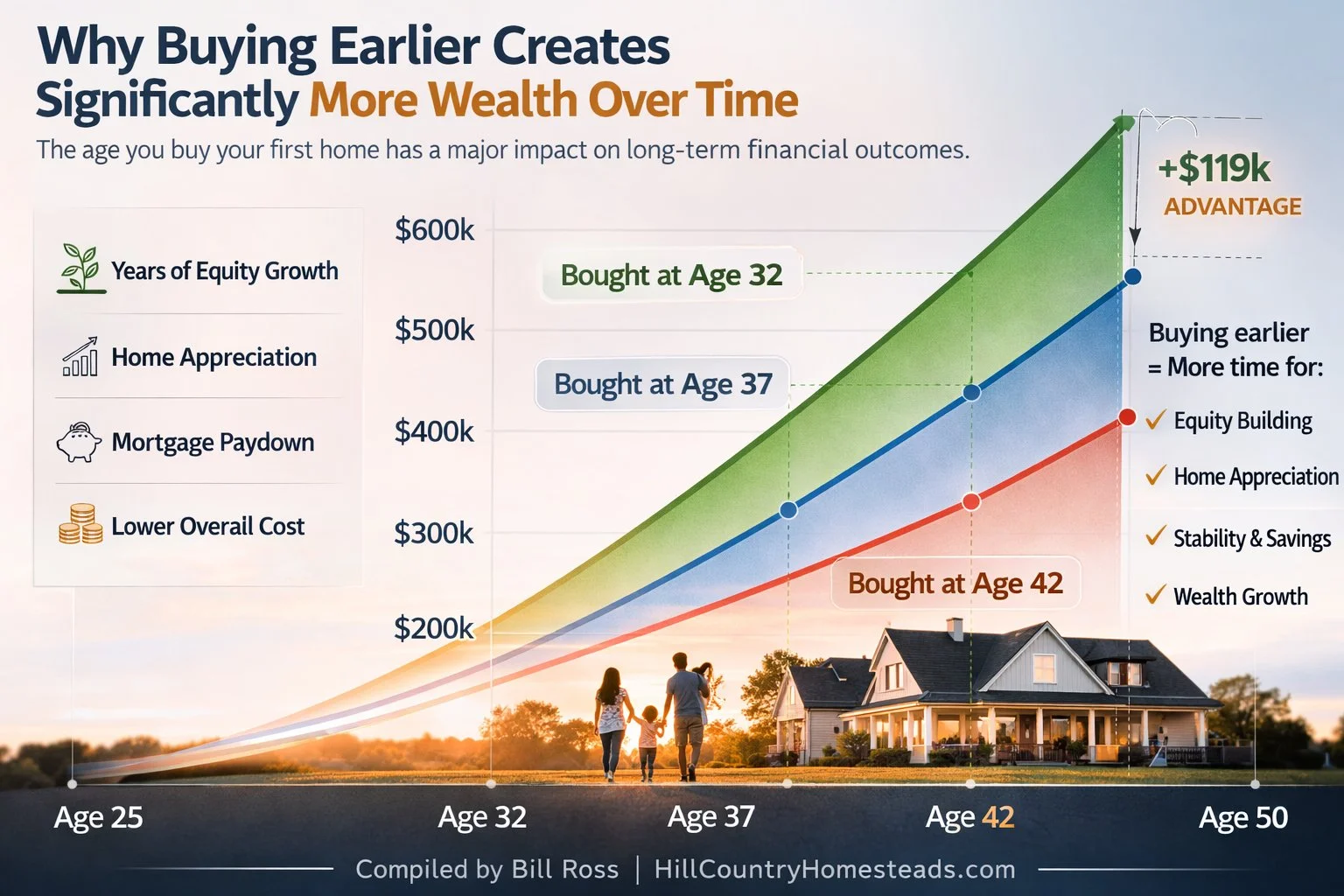

The modern housing market has not made homeownership irrelevant. It has made early entry much harder. That distinction matters. The real divide today is not between people who believe in homeownership and those who do not. It is between households that can get into the market early enough for time to work in their favor and those that are forced to wait while prices, rents, and down payment hurdles keep moving further out of reach. Recent housing research found that buying by age 30 to 32 is associated with materially higher wealth by midlife, while delaying until one’s 40s sharply reduces that long-term advantage. In the same body of research, buying by age 32 was linked to roughly 22.5% higher net worth at age 50, or about $119,000 more, than buying in one’s 40s. [1]

That is the part many people miss. Homeownership is not only about having a place to live. It is also about time. A buyer who gets into a home earlier has more years for appreciation, mortgage paydown, and financial stability to compound. A buyer who waits may still become a homeowner later, but the wealth-building runway is shorter. That does not mean people should buy recklessly. It means the cost of waiting is real, even when waiting feels prudent.

Why First-Time Buyers Feel So Squeezed

The numbers explain why so many young buyers feel like the goalposts have moved. The median age of first-time homebuyers has climbed from 30 in 1990 to 40 in 2025. [2] The same research found that the time required to save for a down payment has stretched from about three years decades ago to nearly 10 years today. [1] According to the National Association of REALTORS®, first-time buyers accounted for just 21% of the market in 2025, the lowest share since NAR began tracking the metric in 1981. [2] This is not a small shift. It means the entry point into ownership is coming later, after years of paying rent, years of missing appreciation, and years of trying to save while housing costs keep rising.

That is why the current market feels so unforgiving. A lot of would-be buyers are not failing because they are irresponsible. They are being asked to do something structurally difficult. They are trying to save for a down payment in an environment where rent is high, mortgage rates are elevated, entry-level inventory is limited, and home prices have outpaced incomes. The traditional path still exists, but it is narrower than it used to be.

What the Data Says About Buying Earlier

One of the clearest findings in the current research is that timing matters more than many people assume. Households that bought at ages 28 to 32 had the strongest midlife wealth advantage. Those who bought at ages 33 to 37 still saw a meaningful benefit, but smaller. By the time households delayed into their late 30s and early 40s, the measurable wealth edge had narrowed sharply. The implication is straightforward: ownership still works as a long-term wealth tool, but it works best when buyers have time for it to compound.

Home Ownership is Generally a Very Safe Investment

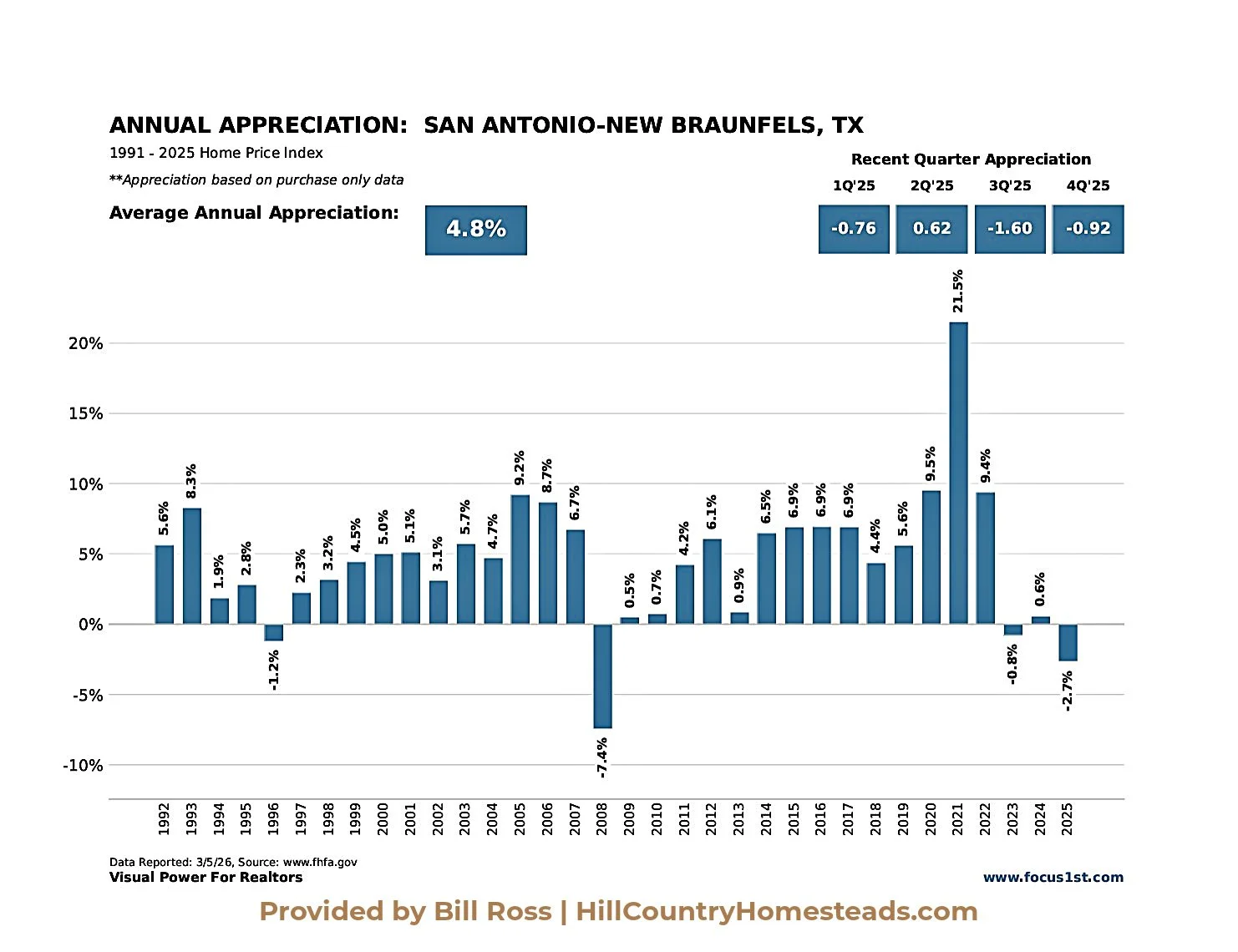

The long-term data on home values reinforces the same principle: time in the market matters. The chart above shows annual home price appreciation for the San Antonio–New Braunfels metropolitan statistical area from 1992 through 2025 based on the Federal Housing Finance Agency Home Price Index. [3]. As with any real asset, there are periods where values flatten or decline—most notably during the 2008 financial crisis and a few recent cooling years. However, the broader pattern is unmistakable: housing values trend upward over time, producing an average annual appreciation rate of about 4.8% [3] across the entire period. That long-term upward trajectory is what allows equity to compound for homeowners who enter the market earlier and hold property over many years. It is also important to recognize that this chart reflects the entire San Antonio–New Braunfels metro area, which includes a wide range of housing markets. Within that broader region, some areas have historically appreciated faster than the overall average. In particular, Texas Hill Country communities such as Boerne and Fair Oaks Ranch have tended to outperform the broader metro market, driven by strong demand, desirable schools, limited land supply, and continued population growth in the Hill Country corridor.

Just as important, the benefits of earlier ownership appear to go beyond home equity alone. The same research found that households who bought earlier tended to accumulate more non-housing wealth as well. In other words, homeownership did not merely substitute for other savings. It appeared to support broader balance-sheet growth. That is one reason the issue is so important for first-time buyers. The question is not simply whether they can buy. It is whether they can buy early enough for ownership to strengthen the rest of their financial life.

Why Parents Are Increasingly Part of the Equation

This is where the conversation becomes more personal. Many parents are now confronting a reality that would have sounded strange a generation ago: even financially responsible adult children often need help getting started.

That help is no longer unusual. According to the National Association of REALTORS®, 22% of first-time buyers used a gift or loan from a friend or relative for their down payment in 2025. Among younger millennials in NAR’s generational report, 33% received down payment help in the form of a gift or loan from friends or relatives. The data also shows that children raised in homeowner households are significantly more likely to become homeowners themselves by age 35. That is not because every homeowner parent writes a large check. It is because housing stability, financial modeling, and family support tend to create a different starting point.

This matters because parents often think in all-or-nothing terms. They assume helping means either funding a huge down payment or doing nothing. In reality, the help can take many forms. It may be a direct gift. It may be a documented family loan. It may be temporary help with rent so a child can save faster. It may be covering closing costs instead of the down payment. It may be helping a child preserve reserves after closing so that buying does not wipe out every dollar they have. The point is not to push adult children into homes they cannot afford. The point is to recognize that modest, well-structured help at the front end may have an outsized long-term impact. The current research strongly suggests that getting in earlier changes the financial trajectory.

The 20% Down Myth Still Hurts Buyers

One of the most damaging ideas in housing is the belief that a first-time buyer must put 20% down. That is simply not true for many loan types. NAR reported that the typical down payment for first-time buyers in 2025 was 10%, and industry research has repeatedly shown that many buyers enter with far less than 20%, depending on the loan program. FHA-insured loans allow eligible buyers to put as little as 3.5% down [4]. VA-backed loans generally require no down payment at all for qualified borrowers, though lenders may impose additional requirements in some cases. [5] Fannie Mae’s HomeReady and Freddie Mac’s Home Possible programs both allow down payments as low as 3% for eligible borrowers.

That does not mean every buyer should aim for the absolute minimum down payment. A larger down payment can reduce monthly costs and strengthen an offer. But the idea that a buyer must wait until they have 20% has sidelined far too many people unnecessarily. In a market where waiting can cost years of wealth accumulation, that misunderstanding does real damage.

Down Payment Assistance Is Real, and Too Many Buyers Ignore It

Many buyers hear the phrase “down payment assistance” and assume it either is not real, is impossibly restrictive, or is meant only for extreme hardship cases. That is a mistake.

HUD maintains a state-by-state homebuying resources page, and FHA remains one of the most widely used low-down-payment paths for first-time buyers. In addition, Fannie Mae’s HomeReady allows flexible funding sources for down payment and closing costs, including gifts, eligible grants, and Community Seconds. Freddie Mac’s Home Possible offers similar flexibility and states that eligible Affordable Seconds can provide 100% of the borrower’s down payment and may also be used for closing costs. For qualified veterans and certain service members, VA loans remain one of the strongest options in the market because they generally allow no down payment and do not require private mortgage insurance.

The practical point is simple: buyers should not assume they have to solve the entire cash-to-close problem alone. Between low-down-payment loans, gifts, grants, employer programs, nonprofit assistance, and state housing agency programs, the real challenge is often not the absence of options. It is the failure to explore them early enough.

What This Looks Like in Texas

For Texas buyers, this is not theoretical. There are real state-level programs designed to reduce the barrier to entry.

The Texas Department of Housing and Community Affairs operates the Texas Homebuyer Program. Its My First Texas Home program offers down payment assistance and 30-year low-interest mortgages for first-time buyers, with certain exceptions for targeted areas and qualified veterans. TDHCA also states that My Choice Texas Home offers down payment assistance and 30-year low-interest mortgages for buyers generally, meaning you do not have to be a first-time buyer to qualify. The program requires an approved homebuyer education course. One TDHCA program page states that My First Texas Home can provide up to 5% [6] of the first-lien mortgage amount for down payment and closing cost assistance.

Texas also has help through the Texas State Affordable Housing Corporation. TSAHC offers down payment assistance in the range of 3% to 5% of the loan amount [7], and in some cases that assistance can be provided as a grant that does not need to be repaid, or as a second-lien structure depending on the program. TSAHC’s Homes for Texas Heroes program is aimed at teachers, first responders, corrections officers, and veterans, while its Home Sweet Texas program is geared toward low- and moderate-income households.

That is why Texas buyers should not walk into the market assuming their only path is to save for years in isolation. In many cases, the smarter move is to sit down with a lender who actually understands state and agency programs, not just conventional loans. The difference between “not ready” and “ready” is often narrower than buyers think.

What Parents Should Think About Before Offering Help

Parents who want to help an adult child buy a home need to think beyond generosity. The right question is not only “Can we help?” It is “How should we help?”

A clean gift is sometimes the easiest path, but not always the best one. Some families prefer a documented loan. Others would rather help with closing costs, reserves, or moving expenses so the buyer can preserve more of their own cash for the down payment. Some may want their child to complete a homebuyer education course first, both to qualify for assistance and to make sure the buyer understands the responsibilities of ownership. Texas programs through TDHCA, for example, require approved homebuyer education for assistance eligibility.

Parents also need to be disciplined enough not to help a child buy too much house. A gift that gets a buyer into a manageable home can be wise. A gift that enables a payment the buyer cannot comfortably carry is something else entirely. The goal should be to improve the buyer’s starting point, not to manufacture a fragile outcome. That is why buyers and parents should work with both a knowledgeable lender and, when appropriate, a CPA or estate-planning professional before transferring funds or structuring support. The family side of the transaction should be as thoughtful as the mortgage side.

What First-Time Buyers Should Do Now

The strongest first move is not house hunting. It is diagnosis.

A serious first-time buyer should find out four things immediately: what price range is actually realistic, what loan programs they may qualify for, whether there are state or local assistance programs available, and whether a family gift or loan could shorten the timeline without creating financial strain. That is how buyers stop guessing and start planning.

This is also where professional guidance matters. A lender who only quotes a standard conventional loan may leave a buyer thinking they need years more savings. A lender who understands FHA, VA, HomeReady, Home Possible, and state housing finance programs may see a path that is invisible in a generic online calculator. In this market, that difference matters.

The Bottom Line

The central lesson is not complicated. Homeownership still builds wealth. The problem is that it now takes more strategy to get started.

For first-time buyers, that means abandoning the fiction that waiting for “perfect” conditions is cost-free. For parents, it means recognizing that a carefully structured assist today may do more for an adult child’s long-term financial future than many people appreciate. And for both groups, it means understanding that down payment assistance is not fringe financing. It is often the bridge between wanting to buy someday and being able to buy responsibly now. The current data makes one thing clear: the earlier households can enter homeownership sustainably, the more powerful the long-term payoff tends to be.

Frequently Asked Questions About Buying a First Home in the Texas Hill Country

Is it better to buy a home early or wait until later in life?

Research consistently shows that buying earlier often leads to greater long-term wealth because homeowners benefit from more years of appreciation and mortgage principal paydown. Even modest annual appreciation can compound significantly over time. While buyers should never purchase before they are financially ready, entering the housing market earlier allows equity growth to begin sooner.

Are there down payment assistance programs available in Texas?

Yes. Texas offers several programs designed to help qualified buyers overcome the largest barrier to homeownership: the upfront cash required for a down payment and closing costs. Programs through the Texas Department of Housing and Community Affairs and the Texas State Affordable Housing Corporation can provide assistance that typically ranges from 3% to 5% of the loan amount depending on eligibility.

Do first-time buyers really need a 20% down payment?

No. Many buyers believe they must save a 20% down payment, but that is not required for most loan programs. FHA loans allow down payments as low as 3.5%, and VA loans for eligible veterans often require no down payment at all. Other programs such as HomeReady and Home Possible allow qualified buyers to purchase with down payments as low as 3%.

How has the San Antonio housing market performed over time?

Long-term data shows that housing values in the San Antonio–New Braunfels metropolitan area have consistently appreciated over time despite occasional short-term slowdowns. Since the early 1990s the region has averaged roughly 4.8% annual appreciation, demonstrating the long-term wealth-building potential of owning property in the area.

Do homes in Boerne and Fair Oaks Ranch appreciate faster than the broader market?

In many cases, yes. While the San Antonio–New Braunfels metro area has shown strong long-term appreciation overall, Hill Country communities such as Boerne and Fair Oaks Ranch have often outperformed the broader market. Strong demand, desirable schools, lifestyle amenities, and limited developable land in the Hill Country corridor tend to support long-term property value growth.

References

[1] Realtor.com Research — Homeownership Accelerates Generational Wealth

https://www.realtor.com/research/2026-generational-wealth/

[2] Federal Housing Finance Agency — House Price Index Data

https://www.fhfa.gov/data/hpi

[3] National Association of REALTORS® — 2025 Profile of Home Buyers and Sellers

https://www.nar.realtor/magazine/real-estate-news/nar-2025-profile-of-home-buyers-sellers-reveals-market-extremes

[4] U.S. Department of Housing and Urban Development — FHA Loan Overview

https://www.hud.gov/helping-americans/loans

[5] Texas Department of Housing and Community Affairs — My First Texas Home Program

https://welcomehome.tdhca.texas.gov/products/my-first-texas-home/

[6] Texas State Affordable Housing Corporation — Down Payment Assistance

https://www.tsahc.org/homebuyers-renters/loans-down-payment-assistance